The first half of 2025 saw a slight increase in company insolvencies with 2,238 registered companies in May 2025, an 8% increase from April 2025 and a 15% rise compared to May 2024. This marks the highest monthly total since June 2024.

Whilst the monthly figures show some fluctuation, the underlying trend points to a continued pressured environment for UK businesses. The 12-month rolling insolvency rate stood at around 53 per 10,000 companies in May 2025.

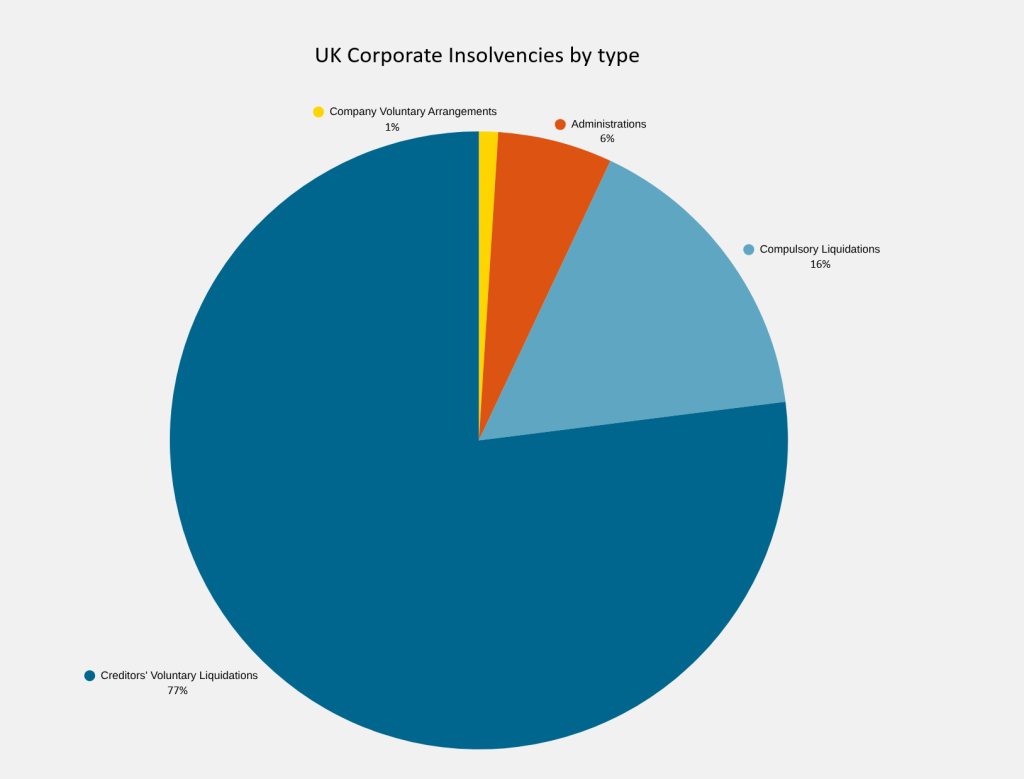

Creditors’ Voluntary Liquidations (CVL’s) were consistently accounting for the largest proportion of corporate insolvencies, making up around 75%-77% of all cases in the first half of 2025. This indicates that a significant number of directors are proactively choosing to wind up their businesses when they become unviable, often due to increasing financial pressure and an inability to meet debts. May 2025 saw 1,734 CVLs, an 11% increase from April and 13% higher than May 2024.

Compulsory Liquidations are on the rise, while CVLs signify a voluntary decision, compulsory liquidations, often initiated by creditors (including HMRC), have seen a notable increase. April 2025 recorded the highest monthly number of compulsory liquidations since September 2014, and while May saw a slight dip, the numbers remained significantly higher than both May 2024 and the 2024 monthly average. This surge suggests a more aggressive stance from creditors, particularly HMRC, in pursuing outstanding debts.

Administrations also saw an increase they aim to rescue a company or achieve a better outcome for creditors than liquidation, have also seen increases. May 2025 saw 136 administrations, up 28% from April and 12% higher than May 2024. This suggests more businesses might be exploring restructuring options, though their numbers are still relatively small compared to CVLs.

Company Voluntary Arrangements (CVAs) continue to be at historically low levels, despite some monthly fluctuations. This could indicate that for many struggling businesses, formal arrangements with creditors outside of liquidation are less viable or less preferred in the current economic climate.

The sectors most affected in the first half of 2025 were:

- Construction: Consistently one of the most affected sectors, grappling with issues like late payments, fluctuating material costs, and mixed weather impacting output.

- Wholesale & Retail Trade: Facing challenges from shifting consumer spending habits, online competition, and increased operational costs.

- Accommodation & Food Services: Continues to be vulnerable to cost increases, staffing issues, and changes in consumer confidence.

- Administrative & Support Services and Manufacturing also feature prominently among industries experiencing higher insolvency rates.

The ongoing financial pressures contributing to these insolvencies include:

- Persistent inflation and high interest rates: While inflation has shown signs of cooling, the cumulative effect of higher costs of borrowing and operating expenses continues to erode profit margins and cash flow for many businesses.

- Increased operational costs: Energy, supply chain, and labour costs (including National Insurance contribution increases) are adding significant burdens, particularly for SMEs.

- HMRC enforcement: The Insolvency Service data highlights HMRC’s proactive approach in recovering outstanding tax debts, leading to an increase in winding-up petitions and compulsory liquidations.

- Weakening consumer confidence: This directly impacts consumer-facing industries, leading to reduced spending and pressure on revenues.

Looking Ahead: The Second Half of 2025

The first six months of 2025 indicate that the UK corporate recovery landscape remains challenging. While there are some signs of a slight stabilisation in the overall insolvency rate on a 12-month rolling basis, the absolute numbers remain elevated, and the surge in compulsory liquidations is a clear signal of increased creditor pressure.

Businesses are advised to closely monitor their financial health, proactively engage with creditors, and seek professional advice at the earliest signs of distress. The focus for the remainder of 2025 will be on how businesses adapt to continued cost pressures and how government and creditors balance support with enforcement.